Your financial plan

is a

living

document.

For driven women, progressive families, and people designing retirement with intention. Planning built to be tested, revised, and refined as your life unfolds.

PhilosophyBefore we touch a spreadsheet, we sit with the personal questions, because a plan that doesn’t reflect who you are will never truly serve you.

Most financial plans start with the numbers. Retirement age. Savings rate. Risk tolerance. We think that’s backwards.

Our approach centers your plan as a living document, your thesis that we revise as your life changes. Who you are is at the core, but how that looks changes over time.

Q.01

"What does enough actually look like for you?"

Q.02

"Who are you becoming — and what will that version of you need?"

Q.03

"What would you do differently if money weren't the constraint?"

Q.04

"What assumptions are you holding about money?"

Q.05

"What does your money say about your values and is it the right story?"

Q.06

"If this plan fails, what will have been the reason?"

"This life is mine alone. So I have stopped asking people for directions to places they've never been."

Glennon Doyle

Who We ServeThree kinds of people.

Infinite variations.

-

Women navigating leadership roles, complex compensation, equity, uneven career pacing, and the emotional weight of being both ambitious and responsible. You may be the primary earner—or on track to be. Either way, you want a plan that reflects your power and your priorities.

-

Families raising kids intentionally, often while supporting aging parents. You’re thinking about childcare, schools, housing, time, caregiving, and legacy—all at once. We help families align money decisions across uneven incomes, competing timelines, stock compensation, career pivots, and big family choices, without defaulting to outdated assumptions.

-

After years of building careers, raising families, and carrying significant responsibility, this stage brings both freedom and uncertainty. You’re rethinking how you want to spend your time, how much structure you still want, and what a well-lived life looks like beyond your professional identity. We help you translate that clarity into a financial plan that supports flexibility, purpose, and longevity; coordinating income, investments, taxes, and legacy planning so your wealth continues to hold what matters most.

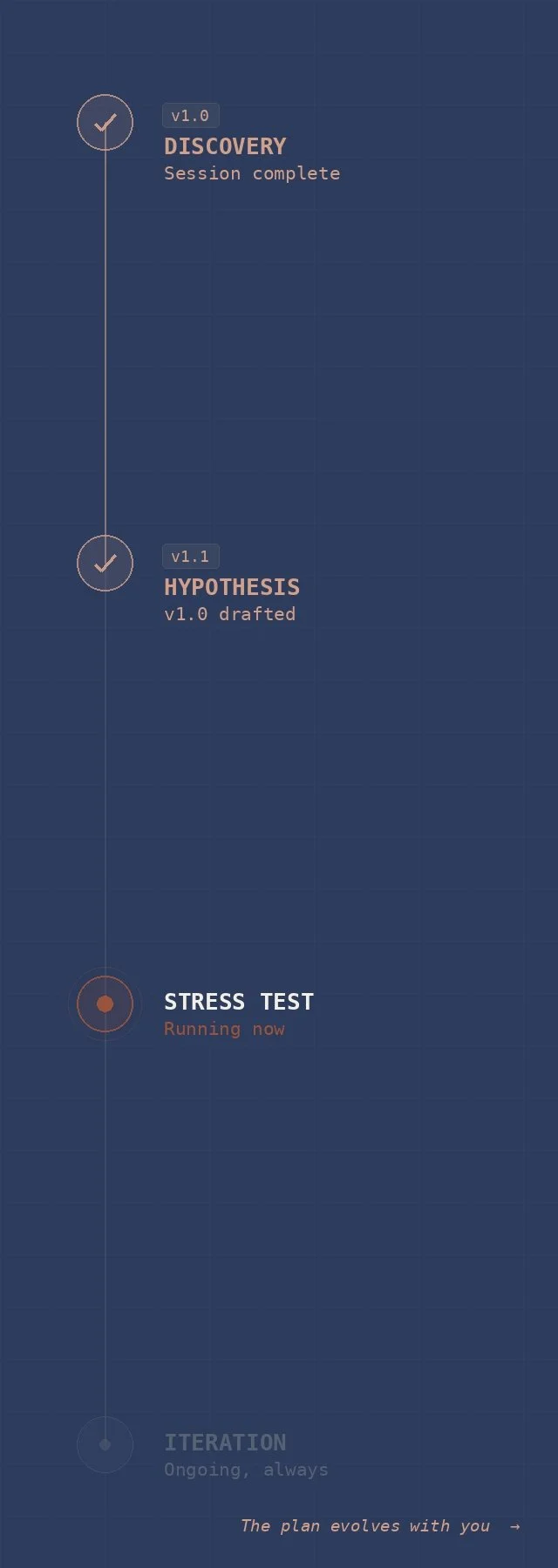

Our processPlanning as

iteration,

not destination.

Life-First Financial Planning

Ideate for the long term.

Less noise, more agency.

01. We work only for you - full stop.

Fee-only. Fiduciary. No commissions, no product sales, no hidden incentives. Advice for you, always.

02. Your values are the key, not a footnote.

Your principles are not up for negotiation and they should shape what you do with your resources.

03. We hold your plan lightly, on purpose.

As with any good thesis, it is meant to be revised as new information surfaces.

04. Progress over perfection.

Momentum is built through action, and we expect to course-correct.

Investment Management

Invest globally, align with your plan, and build to last - that’s our investment philosophy.

01. Diversification is the key.

In a world that feels uncertain, diversifying holdings - globally - is the only honest hedge.

02. Markets are efficient, but it helps to be thoughtful.

Constructing your portfolio with intention and a view towards economic conditions protects on the downside and participates in the upside.

03. Time in the market is worth harvesting.

Staying invested for the long-term while having reserves for short-term needs.

04.Permanent loss of capital is riskier than short-term volatility.

Fluctuations happen. We’re in it for the long-term. Decisions made in panic rarely serve the long term thesis.